Before this, we’ve spoken about the two main types of risk that you’ll have to deal with when you start investing/trading. Right now, we will look into two mathematical concepts that are used in investment/trading which are variance and covariance. These two concepts are useful in itself, and we’ll explain how later — but to give you more context, these two concepts will be useful once you’re talking about evaluating the level of risk for your whole portfolio.

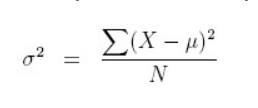

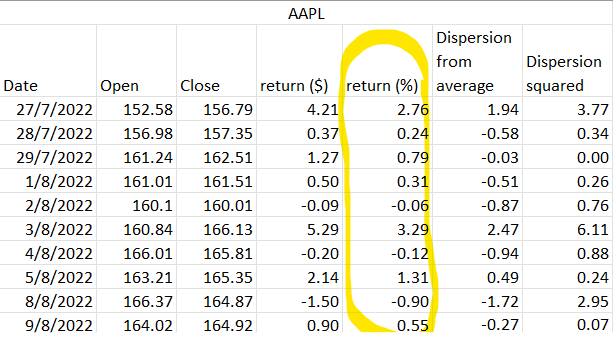

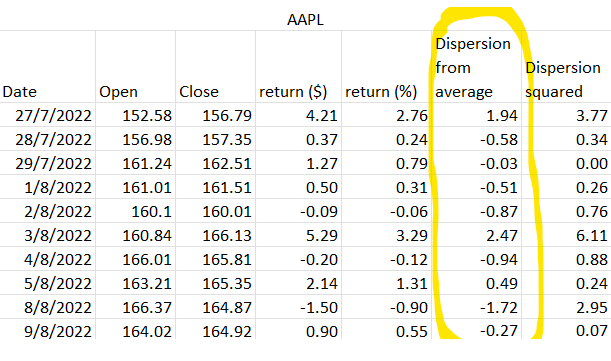

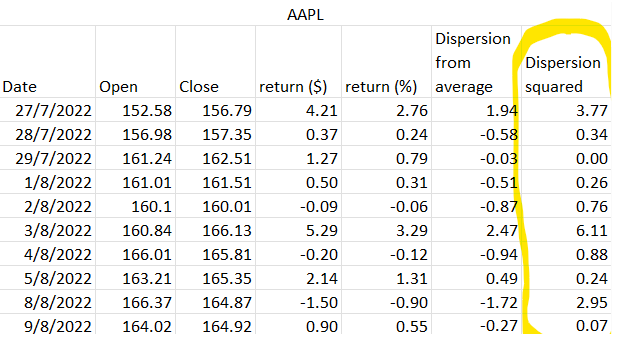

We’ll lay it down simply. The variance would usually tell you how an individual stock is doing, particularly how the returns (usually daily returns) would spread from the average expected returns. It tells you if an individual stock is a nutjob and would stray often from the objective, or if it’s a calm and collected piece of stock that would just linger around your target.

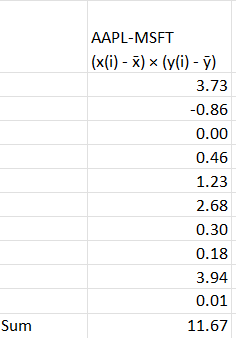

As for covariance, we actually wrote an article specifically on this once. We’ll try summing it in this article, but just to let you know, covariance tells you how one stock relates to another. For example, if Stock A moves up by 1%, will Stock B move up as well? If it does, by how much, and if not, how far apart will they move? This is particularly important when creating a portfolio. If you pick two stocks with a covariance of 1, for example, each stock is valued at $50. If Stock A falls by 10%, there is a high chance that Stock B will also fall by 10%. Most people would wanna balance out their stocks so that their portfolio is not lop-sized.

Here’s the question, covariance works if you’re comparing two stocks, right? Who on earth has a portfolio with only two stocks? Maybe some of you might, but a normal portfolio would have around 15–25 different stocks. How are you going to use variance or covariance on all of them? By using the variance-covariance matrix! But we won’t be touching on that yet, it’s lengthy and we’ll need time to prepare (mentally as well) for it.

For now, we’ll just waddle around variance and covariance.