The whole point of diversification is to look for companies with different levels of risk exposure, or ones that are exposed to different types of risk. The reason behind it is to ensure that if there is any unfortunate development in the market, some of the assets in your portfolio might be taking the fall, but not all of it.

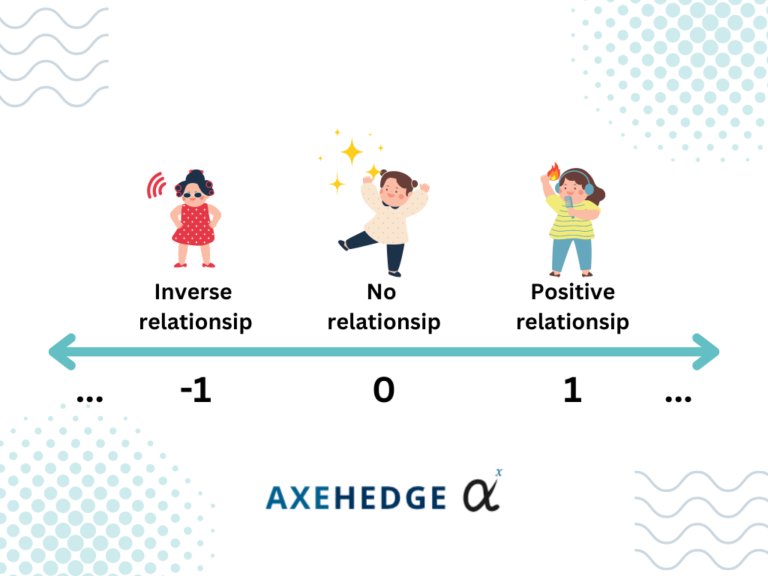

As mentioned above, there are 3 types of covariance, what you want is to make sure that the companies in your portfolio have a covariance that is closest to 0, that is to make sure that they’re not interrelated at all (if that is possible).

Why? The whole point of diversification is to make sure that your portfolio will not crumble upon one bad stroke of luck.

Here’s an analogy: There’s a person with a gun who’s going to shoot you one time, the rule is that the bullet will definitely hit, but the person isn’t a very good shot, so the impact location is randomized. Should you cuddle up into a ball or just spread yourself wide open?

In this case, one bullet will definitely hit you, but the location is randomized. In this situation, it’s not wise to cuddle up into a ball, as many of your vitals will be closely packed together.

So, if the bullet hits, it might pierce through and damage your vitals which are closely located to each other. We know that this isn’t the best way to put it, but as long as the point comes across.