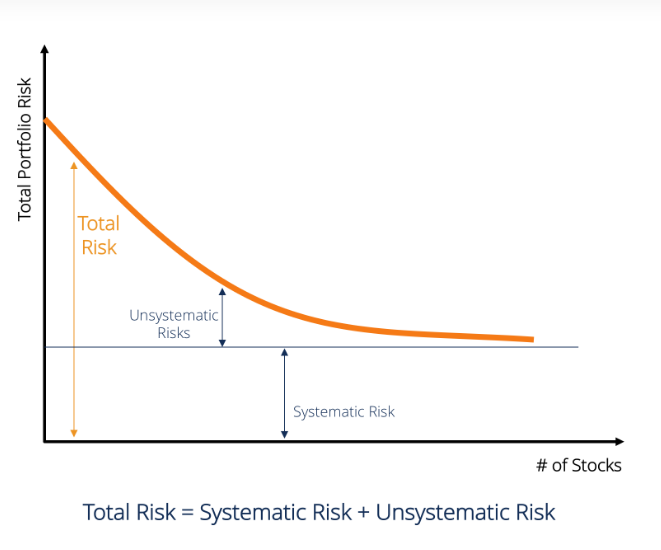

On the bottom axis, we can see that as the number of stocks in your portfolio increases, the total portfolio risk decreases — but it would stop decreasing at some point. Here’s what happened, when you diversify, you reduce the unsystematic risk. So, you reduce it, and reduce it, and reduce it, but think with this common sense: is there any investment without risk at all? Impossible, right? Unless if you’re talking to a scammer.

The risk that is left afterward is the systematic risk. That’s why in the graph above (which is from CFI), they laid down the formula: Total Risk = Systematic + Unsystematic Risk.

You can diversify to reduce unsystematic risk, but what can you do to reduce systematic risk?

Systematic risk

When it comes to systematic risk, what you can do to reduce it is through hedging. Should you do it, though, is another issue. So, what is hedging? In a simple way, hedging is much like the hedge you see on your neighbor’s lawn, which stops their dog from pooping on your lawn — it stops risk from coming toward your portfolio.

Sounds good, doesn’t it? That depends, but we’ll get to that shortly. Let’s get to hedging first. Hedging is also like the car insurance you pay. You’ll have to allocate your money by paying the insurance premium over time, but if you get into an accident, the damage to your pocket won’t be so severe because your insurance company will pay for the repairs.

Do investments have insurance as well? In some ways, yes. Let’s take a look at a few things that investors/traders usually do to hedge their portfolios. Some would buy a ‘put’ contracts which is a contract that gives you the option to sell an asset at a specific price over a certain period. For example, you bought Stock ABC at $100, and you bought a put contract that allows you to sell it at $95 within the period of 1 year. If Stock ABC falls to even as low as $0, you can save your portfolio by exercising the put contract and sell it at $95.

Some would also go for assets that move in the opposite direction as their portfolio. For example, if the portfolio goes up, the hedged asset will move down, and vice-versa. This will offset the losses you make if your portfolio goes down. Can it be 0 risk? Theoretically, yes.

If you invest in Asset A and hedge with Asset B where if Asset A moves up by $1, Asset B will move down by $1, and vice-versa. Technically, if your Asset A falls, Asset B will offset the losses, but there will also be no gains in your portfolio, as the end result will always be $0.

Those are only a few examples, and there are many ways to hedge your portfolio. There are also hedging methods that cater to specific risks such as inflation, rate hikes, and even currency fluctuations. However, the question of whether you should do it or not is another issue.

Hedging takes a lot of skills, can be costly, and it requires you to be timely — there’s no one-hedge-for-all. Much like your car insurance, the basic insurance package will cost you, say, $300. If you want to insure your windshields, it will cost you more, and if you want protection against natural disasters as well, you’ll have to add it to the package and pay more.

At some point, you might see your wallet torn apart only by the cost of hedging alone if you are too afraid of risk. That is why hedge funds only cater to rich people — if you are wondering. Even then, they will not try to do a 100% hedge against risk. After all, higher risk = higher returns.

If you’re just starting out, it would be better for you to cater to unsystematic risk by diversifying and just generally be smart and do your research on the trades that you’re going to make. If you want to hedge, be sure that you know how, and that you can keep up with the game.