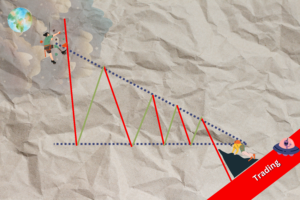

The second triangle: the Descending Triangle

Read More

Here’s the thing tho, making the standard deviation bigger (moving to Tier 2 or Tier 3) doesn’t always mean that it’s good. Of course, there’s a higher likelihood that your portfolio can hit the spot, but this is like casting a huge net and then bragging when you get some fish. It’s not because you know how to fish, it’s just that your net is enormous, it takes in everything, including fish.

When investing, you don’t want to be dealing with a range too big, because you need some accuracy for your predictions. How would these estimates be of any use then?

The key to see if your portfolio’s expected earnings are good or not is by seeing where the bell curve lies. How does that work? Well, in a normal situation, you’d expect a 50–50 situation, where if the lower band is -10, the middle one is 0, and the upper band is 10, like the image below (which is kinda ugly, sorry).

The image above is a normal situation. If we look at it in a sense of risk-taking, you bet $10 so that you can either gain or lose $10. It’s a ‘fair’ 50–50 game. In our portfolio’s case, however, it looks more like this:

Right now, the middle point is no longer zero, which means that the curve has moved to the right. To understand this, we’ll move away from finance and look at this simple example:

Students from 4 schools will answer the same examination paper. Assuming that each school performs in a way that fits the bell curve pattern, can you identify the school that performs the best?

The answer is that School D is most likely the best school when it comes to the examination that they just had. Why? Because most of its students score on average more than other schools’ average. Their lowest band is at around 60%, which means that their students are quite the brainy bunch.

5 Common Mistakes Beginner Traders Make

Things to avoid when you’re just starting to trade

Read More

Trading Dow Pattern the Triangle Pattern (Part 1)

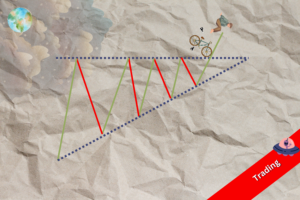

The first triangle: the Ascending Triangle

Read More

Funds: Equity Funds (Part 3)

How to choose between equity funds based on companies’ earnings...

Read More