The second triangle: the Descending Triangle

Read More

We won’t be discussing in detail how to do it, if you’re interested to know how to do it, you can head over to our article below:

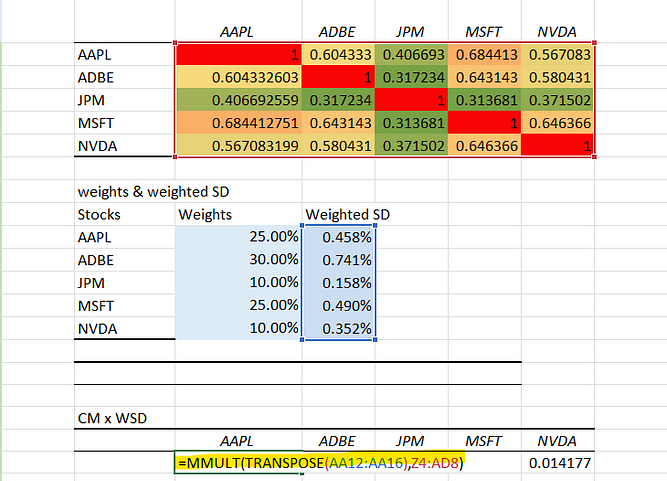

Risk management: Correlation Matrix

From the previous calculation, we have this as our Correlation Matrix:

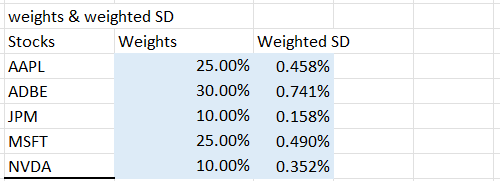

The weight of the stock in your portfolio is simply how much percent of your total portfolio value the stock contributes to. If you have $1,000 in terms of Portfolio Value and Stock A’s value is $100, then Stock A’s weight is 10% in the portfolio.

Weight = Stock Value / Portfolio Value * 100

From our previous calculation, we assign these weights to our stocks:

Note: We just made the numbers up. When actually doing it, be sure to calculate it properly.

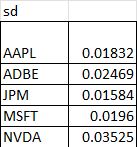

To do that, you must first calculate the Standard Deviation for each stock’s return. We do it in MS Excel using the =SDEV function and then highlight all the returns for a particular stock.

This is what we came up with:

The formula for Weighted Standard Deviation (Weighted SD) is as follows:

Weighted SD = weight of a stock * standard deviation of a stock

Now that we already have both the weights and the standard deviation, this is the result:

Now, select an empty space in your MS Excel file and create the ‘placeholder’ for the result. It would look something like this:

Now, highlight all of the empty space (from AAPL to NVDA), insert the following equation:

=MMULT(TRANSPOSE(range of Weighted SD), range of the Correlation Matrix)

In our case, it would look something like this:

This is how the result would look like:

Select any empty space in your MS Excel sheet, and use this formula:

=MMULT(range of value in CMxWSD table, range of value for weighted SD)

This is the result that we get:

0.000326514

5 Common Mistakes Beginner Traders Make

Things to avoid when you’re just starting to trade

Read More

Trading Dow Pattern the Triangle Pattern (Part 1)

The first triangle: the Ascending Triangle

Read More

Funds: Equity Funds (Part 3)

How to choose between equity funds based on companies’ earnings...

Read More