The second triangle: the Descending Triangle

Read More

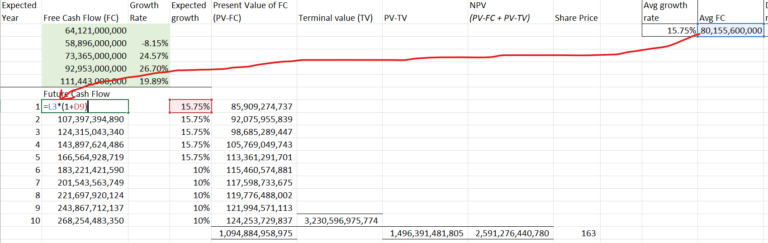

This article is a part of our series on how to choose your stocks for investment using fundamental analysis. Terminal value is a component under the third stage of the analysis, which is known as Discounted Cash Flow (DCF). As a quick recap, there are three stages to fundamental analysis (generally speaking).

The first step is to look at the business overview to get a first glance at how the business is doing generally. If they pass the test, move to the next step and apply financial ratio analysis on these stocks to see if it supports your initial findings. If this step is passed, move on to the last step, which is to look at Discounted Cash Flow (DCF) to see if the price that you’ll buy it at is worth it or not.

We are now at the last step. However, mind you there are a few core concepts that we’ll need to master before we can actually jump into the DCF evaluation. In this article, we will learn the third concept which is the terminal value.

5 Common Mistakes Beginner Traders Make

Things to avoid when you’re just starting to trade

Read More

Trading Dow Pattern the Triangle Pattern (Part 1)

The first triangle: the Ascending Triangle

Read More

Funds: Equity Funds (Part 3)

How to choose between equity funds based on companies’ earnings...

Read More