In a span of six months, Walt Disney’s stock has lost over 37.62% of its value and is down around 47% from its all-time high in March 2021. Despite Disney’s (DIS:US) stock’s slide and lack of a dividend (after they cut off the semi-annual payout in 2020), there’s reason to believe there has never been a better time to buy. Here’s why.

The Walt Disney Company is a worldwide entertainment giant that owns theme parks, movie studios, television networks, streaming platforms and more. The current share price now is where the theme parks were closed during the pandemic in 2020. Now, due to the subdue covid condition, the theme parks are packed. Along with that, Disney +, the biggest driver for the stock stability recently had seen additional subscribers compared to its competitors – NETFLIX. The streaming features are currently available in 80 countries and will continue soaring to 80 more.

Major financial institutions such as Credit Suisse Group, Daiwa Capital Market, Tigress Financial and more highlighted the “BUY” sentiment on Walt Disney’s shares with a targetted projection price range of $151 to $229. In addition, Disney’s newly released crossover game, Disney Mirrorverse adds to Disney’s pocket flow. The game alongside Disney and Kabam lay out a fictional universe to other Disney canon, featuring universe from Disney, Pixar and other characters from different franchises re-envisioned in a new storyline. On the released day,- it shows a 6.08% increase in Disney’s share price.

Amazon is down 31% YTD. Macroeconomic obstacles will continue to hinder its operations. Fuel prices continue to grow, which means shipping costs are also on the rise. On June 6, Amazon (AMZN:US) completed a 20-to-1 stock split. Is Amazon still a buy?

Amazon remains the largest e-commerce space and as people return to a new normal, the business should follow. It is poised for a strong earning towards the end of the year as we approach the busier shopping seasons of fall and winter.

Amazon’s biggest profit region is actually its cloud infrastructure unit, Amazon Web Services. This has provided Amazon with an impressive profit margin of 35%, and it is just the beginning. Amazon’s cloud infrastructure business is so potent, to the point that when Jeff Bezos stepped down as CEO, he was replaced by AWS architect Andy Jassy.

Amazon has an average Wall Street price target consensus rating of $180.13 (a 45% upside potential).

Nvidia Corp’s stock has lost over 43.14% of its value and is down around 50% from its all-time high of $346.47 in November 2021. Nvidia (NVDA:US) is the titan player of is a giant in data center and gaming along with chips that power the future of self-driving cars and cryptocurrencies. Nevertheless, it still suffers from price crashes over a span of 6 months. We still believe that NVDA is a good stock to splurge on. Here’s why.

The data center business became Nvidia’s largest source of revenue with $3.75 billion in revenue last quarter and the gaming business, was its second-largest business with $3.62 billion in revenue last quarter. Nvidia had just launched Omniverse Cloud last march 2022, a suite of services that gives artists, creators, designers and developers instant access to the nascent Nvidia Omniverse platform. Joining the metaverse bandwagon, Nvidia is targeting business along with another major player like Meta.

With more businesses harnessing cloud computing and artificial intelligence (AI), data research will continue growing for years. According to Nvidia CEO and founder, Jensen Huang, Nvidia’s Data Center demand is strong and remains strong. Furthermore, when the omniverse or self-driving technology takes off, the segment could project massive growth. Not to forget, in the gaming sector that has driven the branding of Nvidia, gamers will always demand the latest technology, thus, the demand for the segment will be in constant growth.

Meta’s shares lost nearly half their value in six months. Both Google’s Android and Apple’s changes in privacy policy dented digital advertising and were one factor behind Meta’s catastrophic earnings. But Meta’s (META:US) CEO Mark Zuckerberg isn’t worried at all. Mark Zuckerberg is committed to spending tens of billions of dollars to build the metaverse over the next decade.

Wall Street continues to be mostly bullish on the metaverse as well, with some top analysts and hedge fund managers arguing it’s the most important invention since the iPhone and will end up being worth trillions.

“I’m just trying to lead the company in a way where we’re positioning ourselves as the premier company for building the future of social interaction and the Metaverse,” – Zuckerberg.

Prior to the COVID-19 pandemic, Etsy was growing smoothly and steadily by bringing together crafty makers and consumers seeking something out of the ordinary. But it all changed during the pandemic when travel restrictions and contact minimization gave a boost to all e-commerce platforms. Etsy (ETSY:US) in particular, absolutely skyrocketed, growing at more than twice the rate of overall e-commerce. In the span of under two years, shares of this digital retailer soared over 550%. They eventually reached an all-time high of $294.

Etsy had recently released its Q1 earnings report. Many investors lost interest in the stock because the outcomes weren’t fantastic. Etsy reported $579.27 million in quarterly revenue, an increase of barely 5% year over year. Additionally, it reported an $86.1 million total profit, a 40% YoY decline. This profit amounts to roughly 60 cents per share, which is certainly not the best quarter of all time for Etsy.

But it’s crucial to keep in mind that the epidemic caused Etsy’s expansion to pick up speed. It reported a 200 per cent year-over-year increase in net income for FY 2020. Naturally, growth couldn’t continue at this rate. That would be incredible. Etsy’s stock is just now beginning to climb at its usual rate and because of its platform and brand strength, Etsy’s market opportunity is in the hundreds of billions of dollars, and it has just started to scratch the surface.

Over the last decade, Spotify has dominated the music streaming industry. Spotify’s popularity is due to its personalized music suggestions and simplicity in finding new artists, according to its 422 million monthly users.

Analysts had previously pointed out subscriber churn rate as a reason to avoid putting your money in these media streaming services. Many companies have been dealing with this issue, thanks to rising membership costs. But despite increased competition with the likes of Apple Music and others, its subscriber churn has fallen by 30% with its low price had helped it keep subscribers on the platform. An improved revenue outlook may also put Spotify on the right track. Gross profit had tripled over 3 years, growing at a compound annual growth rate (CAGR) of 35%. Daniel Elk, Spotify’s CEO, estimates the company will see a 40% improvement in its gross margin and a 20% improvement in its operating margin.

Competing with other large tech companies is very difficult, but Spotify (SPOT:US) had shown clear dominance over other players in the audio streaming industry. The platform strives year after year and is reflected in the company’s earnings results. Hence, we believe long-term investors, who like tech stocks, should go and take a look.

Tesla Inc’s stock slide almost 39% of its value and is down around 41% from its all-time high of $1243 in November 2021. Not to overshadow by Elon Musk’s (Tesla’s CEO) recent obsession with Twitter Inc, the electric vehicles (EVs) titan company doesn’t change the fact that Tesla’s vehicle production is increasing quickly, and revenue and profit are both climbing.

Last August 2020, Tesla (TSLA:US) announced a 5-for-1 stock split, and the share price soared above $2,000, paving the way for it to join the trillion-dollar club. Last June 10 2022, Tesla filed paperwork for 3-1 stock split which Shareholders will vote on a 3-for-1 stock split at the 2022 Annual Meeting of Shareholders next August 4 2022.

“Tesla is a lot more than a car company and we are, in my view, the leading real-world AI company that exists,” Musk said. Following suit, Tesla to release a prototype of its humanoid robot next September 30, 2022. Tesla will begin production of Optimus in 2023. With a target projection of $887.22, Tesla is still on “Moderate Buy”.

Starbucks is down 33% YTD and is now trading at a historical low P/E of ~20. With rising levels of inflation exceeding 8%, Starbucks (SBUX:US) will inevitably be hit. Its coffee beans are not homegrown. They are sourced globally. Coupled with supply chain bottlenecks in the global shipping market, the cost of transporting coffee would increase as well.

However, with its superior brand loyalty, it might be worth keeping an eye on the fundamentals.

The company is planning to raise prices again, the third hike since October 2021. While its products are considered a “luxury” item to most consumers, it maintains a strong customer loyalty due to the fact that morning coffee is now a daily routine for many.

Howard Schultz, the former CEO recently returned to helm Starbucks just four years after leaving. Schultz masterminds its rise to an international chain and is committed to tackling Starbucks’ problems head-on.

Starbucks pays an annual dividend of $1.96 per share and currently has a dividend yield of 2.51%. Starbucks has been increasing its dividend for 12 consecutive years, indicating the company has a strong commitment to maintaining and growing its dividend. For long-term investors, they would have made 6%, each year, over five years.

So, what’s the worry.

There are currently 13 hold ratings and 13 buy ratings for the stock. The consensus among Wall Street equities research analysts is that investors should “moderate-buy” Starbucks stock.

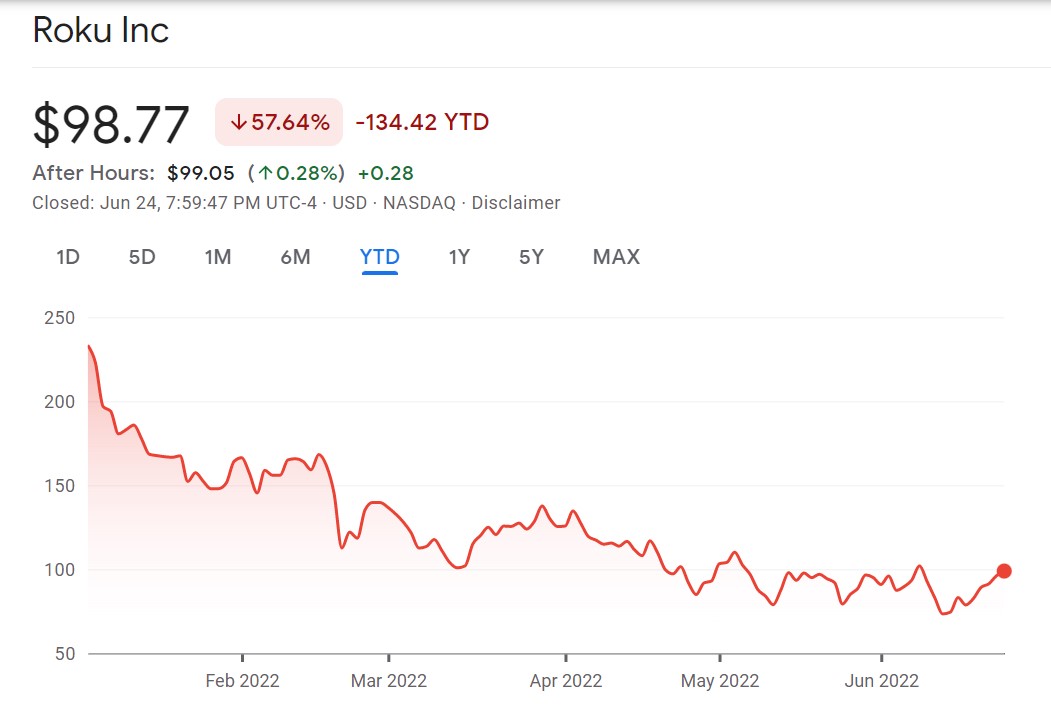

Once upon a time, shares of Roku were once up over 600% since the pandemic began as investors flocked to the possibility of video streaming platforms, but the company has subsequently fallen and is now down 60% year to date. Investors are concerned about declining margins and sluggish account growth, two important business metrics for Roku (ROKU:US).

But the valuation of the streaming-TV platform specialist is starting to look cheap. Although Roku may look expensive at 88 times earnings, bear in mind that this is a true behaviour of a growth company. Further, Roku continues to grow fast, as evident from its Q1 earnings results which saw revenue increase 28% over the year and are expected to have a strong second half of 2022. Roku’s management guided for 25% top-line growth in Q2 but 35% growth for the full year.

The strong outlook is due to the fact that the company has easier YoY comparisons in the second half of the year. Given its growth opportunity and valuation, we believe that Roku shares can perform well moving forward, especially in the long run.

Paypal is down a whopping 60% YTD, a percentage that is roughly double as much as what the Nasdaq 100 index has shed during the same period. The collapse is due to a confluence of various negative macroeconomic conditions as well as company negative developments. An increase in interest rates in the US, competition in the digital payments landscape and inflation led to a slowdown in consumer spending.

PayPal is one of the 30 most popular stocks among hedge funds and was in 100 hedge fund portfolios at the end of the first quarter of 2022.

At its core, PayPal (PYPL:US)l remains a digital payments stock but appears to be positioning itself across a number of fintech verticals, including e-commerce, banking, and crypto/blockchain. The company also owns the popular Venmo mobile app. Venmo is the preferred payment app for many young people and is popular with gig workers.

Also, if you want to make a small bet on crypto but don’t want direct exposure, PayPal is one way to hedge your bet.PayPal remains an excellent long-term buy. The worst is likely over.