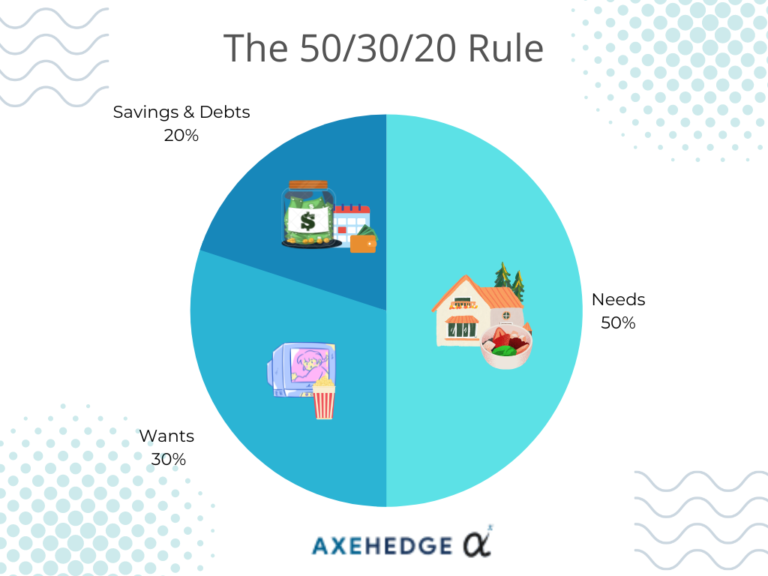

Frankly, if your income is relatively low and paired with the high cost of living, it is not a perfect plan. However, you don’t always have to follow this rule strictly – create some wiggle room to allow your money to grow.

Say, you make below-average in San Francisco with $4,000 a month (after tax) and you’re renting an apartment with a $1,500 monthly. You pay $540 for your car and around $360 monthly for groceries. The total is around $2,400. That is already 70% of your income.

Now, you’re left with only 30% of your income instead of 50%. Is it a sign to say “nope” and just abandon it? No.

What to do then?

We suggest that you adjust your ratio according to the balance of income. Say, from the example above – you’re now left with 30% of your income.

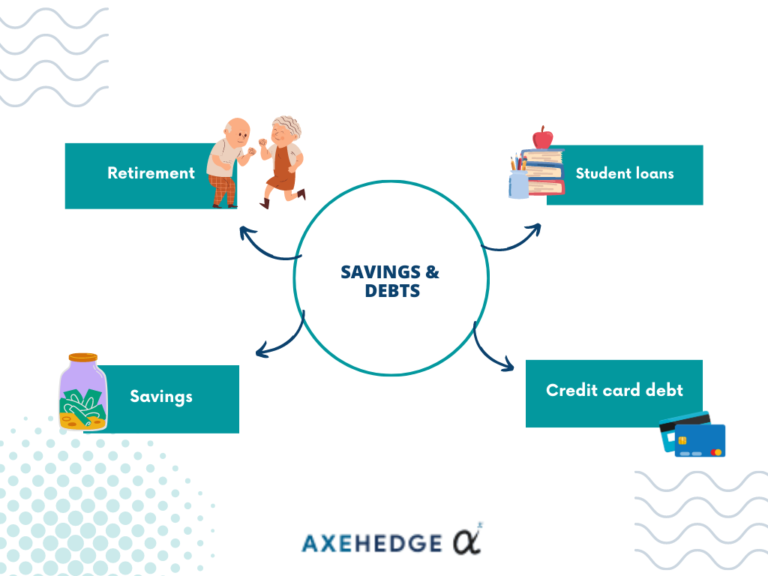

Since needs are not something you can compromise with (you can’t decide to say no to paying for food), what you can do is compromise with your wants or even investments, but we don’t recommend you compromise with debts.

A prolonged debt wouldn’t be good for your wallet, especially when some of them entail interests that grow at a worrying rate. When we speak of compromising investments, we don’t mean that you should leave it out.

Instead, you can reduce the allocation of your income that you’d use for investments. The key is to not abandon it all but invest as much as you can, even if it’s just a dollar.

Or you could also explore other allocation methods like the 80/20, zero-based, and envelope methods.