The second triangle: the Descending Triangle

Read More

The market rejoiced well at the news, given how the CPI data will greatly affect the Feds’ decision on whether to raise interest rates further. As it stands, the Feds have already hiked interest rates four times in 2023, starting from a hike to 4.75% in February to now 5.5% in July. There was only one time that rates were not raised, which is in June.

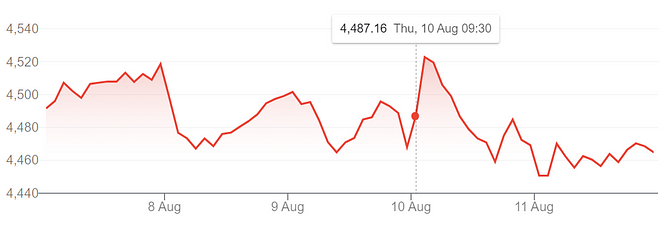

The market’s gleeful response can be seen when the S&P 500 index rose by 0.79% in the span of just half an hour after the market opened. Alas, the joy was short-lived, and the S&P 500 fell by almost 1.18% from its peak to the day’s close.

The question is why? Why did the market respond in such a way despite relatively well data being released?

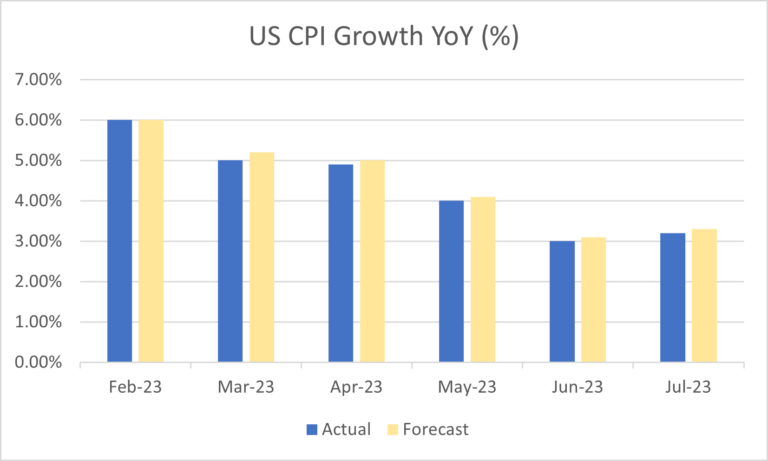

Later on in the week, which is on Friday, if we are to be exact — the market saw two major data releases that brought them to really rethink their optimism. First, the YoY Producer Price Index (PPI) which measures the change in the price of goods sold by manufacturers rose more than anticipated in July, mainly due to a rebound in service costs, suggesting a mild moderation in inflationary pressures.

US PPI YoY in July rose to 0.8%, higher than the expected 0.7%, and a massive increase from the previous month’s 0.2%. Despite that, goods prices excluding food and energy remained stable, indicating a continuing trend of reduced inflation in goods.

At the same time, US Consumer Sentiment data by the University of Michigan was also released. Confirming the anxiety of the market, consumer sentiment declined in mid-August but remained significantly higher than a year ago. The initial consumer sentiment index reading dropped to 71.2 in early August from 71.6 in July, below the predicted 71.7.

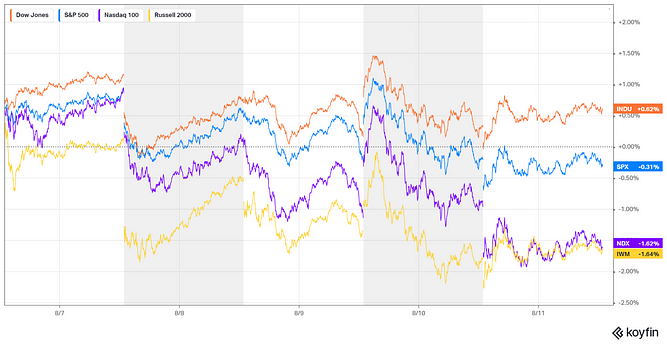

Global stocks then dipped while the U.S. Treasury yields rose, leading the market to brace for prolonged higher interest rates by the Feds. The bond market’s reaction to inflation caused a ripple effect on stocks. The Dow rose 0.62%, the S&P 500 fell 0.31%, and the Nasdaq Composite dropped 1.62%.

These past few months have seen AI rallying at a pace that can only be beaten by Chuck Norris’ sheer will. Jokes aside, we might be finally seeing the market comes to its sense as to the real prospect of AI. Not that AI was a mistake, on the contrary, AI will be big as it seems. The key phrase here, however, is “will be”.

The massive rally, especially one that Nvidia saw, was arguably a bit too much. It’s like that time when anyone could talk about was of either Barbie or Oppenheimer. Sometimes the hype precedes the real growth, and such can be said of AI.

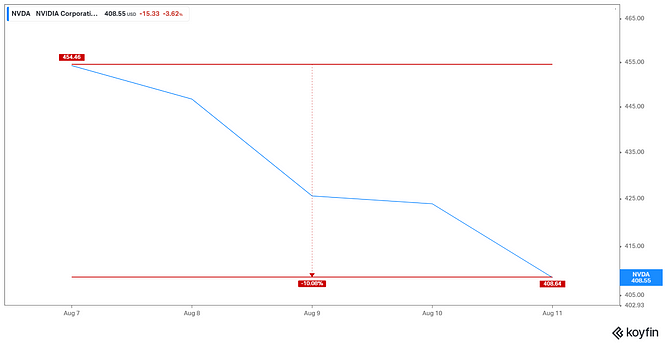

Throughout the week, Nvidia saw its share fell by more than 10%, a move that one could argue as a correction.

However, this doesn’t mean that AI is dead, nope. This is the moment where the real momentum can be seen. Much like in a swimming race, the first few meters are just ‘hypes’ created by a swimmer’s jump, the real show of strength is after the hype ends, and this is where AI must swim or sink.

Spoiler alert: They will swim, by the way. It’s just a matter of who will swim forward and who will sink.

5 Common Mistakes Beginner Traders Make

Things to avoid when you’re just starting to trade

Read More

Trading Dow Pattern the Triangle Pattern (Part 1)

The first triangle: the Ascending Triangle

Read More

Funds: Equity Funds (Part 3)

How to choose between equity funds based on companies’ earnings...

Read More