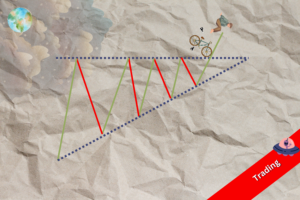

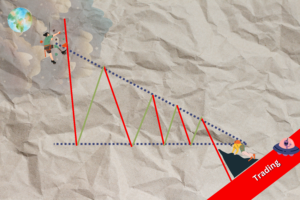

The second triangle: the Descending Triangle

Read MoreThere will be no hustle and bustle on Monday, at least none in terms of stock movements as the US celebrates Martin Luther King Jr. Day and the market will have its shutters down for the day. Nonetheless, here are the market updates we tailored especially for you!