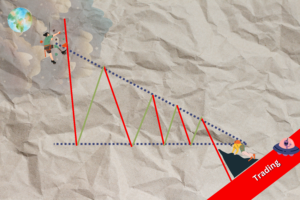

The second triangle: the Descending Triangle

Read More

5 Common Mistakes Beginner Traders Make

Things to avoid when you’re just starting to trade

Read More

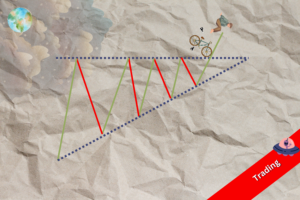

Trading Dow Pattern the Triangle Pattern (Part 1)

The first triangle: the Ascending Triangle

Read More

Funds: Equity Funds (Part 3)

How to choose between equity funds based on companies’ earnings...

Read More