Whilst the Alpha is commonly used to measure fund performance together with excess returns, the definition of Alpha can be also utilised to identify a manager’s skill in managing the fund or investment. In another perspective, the skill of a manager also reflects the ability of her generating excess returns (vis a vis a benchmark) given the level of risk taken. Taking risk into account for investment allows us to peer beneath the veil to better understand how returns are generated by the manager. With a bit of mathematical work, alpha provides investors better clarity and context to a manager’s ability to generate performance.

Before we go further, consider the following formula:

Where:

The formula above simply explains how investors can calculate alpha, typically referred to as Jensen’s Alpha. This exercise allows us to better understand a fund manager’s performance against returns to that of another market-related investment (i.e., a fund managed by another manager), whilst considering a fund’s correlation to the market (denoted by Beta). In the case of Beta, a value greater than 1 (β>1) would indicate that an asset or fund brings greater levels of risk and implies greater gains (or losses) in times of large market swings or uncertainty.

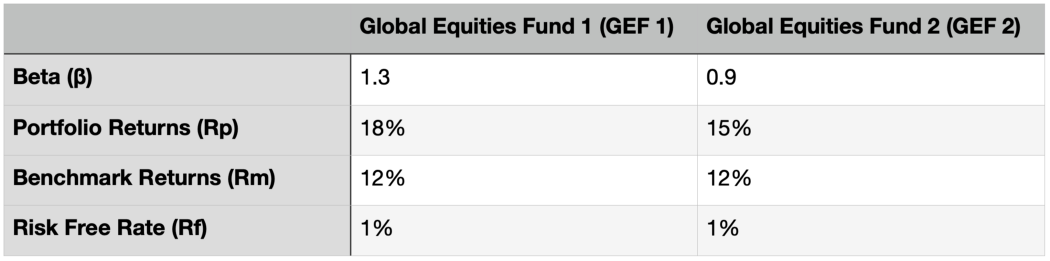

Now that we have a grasp of how alpha can be used to measure a manager’s ability to generate superior risk-adjusted returns, let’s see how this concept can be applied to the following example:

Note that:

- At first glance, an investor might be tempted to select GEF 1 as it generates superior returns, whereas GEF 2 might not be as attractive since it lags slightly behind GEF 1 in terms of performance; and,

- Notice that the Beta value (an indicator of risk) for GEF 2 is significantly lower than GEF 1, implying that GEF 2 is less susceptible to large fluctuations in times of market stress.

By calculating the value of alpha, we now have better clarity over which fund is more superior:

Based on the calculated results above, we conclude that despite the impressive returns reported by the first fund (GEF 1), it has a lower alpha value as opposed to the second fund (GEF 2). This also posits that the Manager of the latter fund is more adept at generating superior risk-adjusted returns when comparing the Alpha values for both of the funds.

To summarise, whilst the manager for GEF 1 is capable of generating greater excess returns, it achieves this at the expense of excessive risk-taking. By comparing the Alpha values generated by both funds side-by-side, we can peer beyond the fund’s performance and single out the manager’s ability to produce excess returns for a particular risk level.

In the never-ending search for Alpha, is active management still relevant? In short, it’s complicated, but let’s break it down. The proliferation of actively managed funds has been in existence since the advent of the Cold War, where investors stock-pick and select the best equities (blue-chip stocks) in hopes that the appreciation of these assets would grow in tandem with the global recovery. This later proliferated into a booming industry where managers would employ fundamental analysis, together with the birth of modern-day financial theories to explain phenomenons surrounding the capital markets. Fast forward today, active managers face a new challenge arising from the opposite end of the asset management spectrum — passive management.

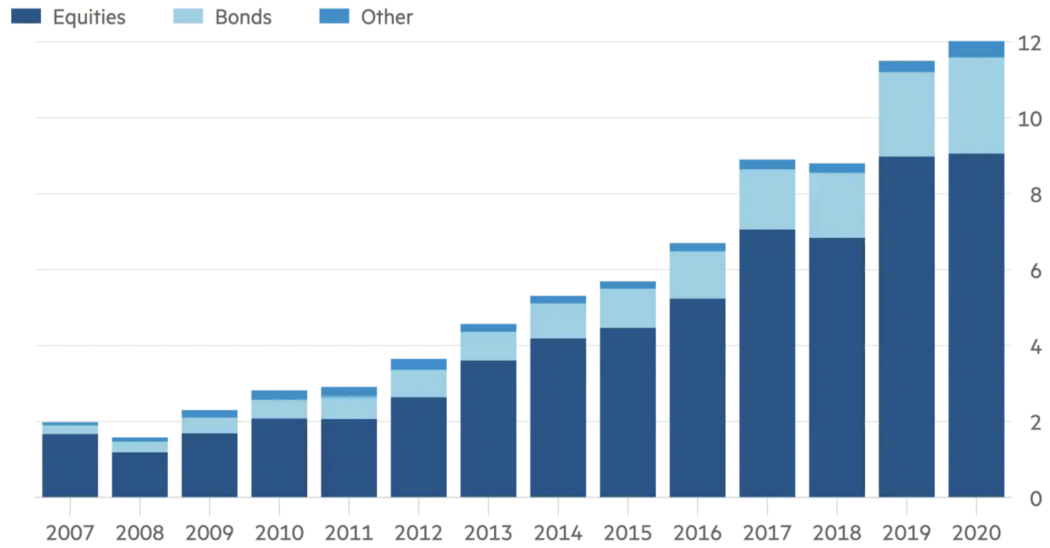

Figure 1: Total net assets (by asset classes) for passive managed fund universe (Source: Morningstar, 2020).

Figure 1: Total net assets (by asset classes) for passive managed fund universe (Source: Morningstar, 2020).

The performance for active and passive management is nearly indistinguishable for the past two decades as suggested by recent literature. Where passively managed funds tend to perform during periods of economic boom, active funds tend to thrive better during times of market volatility. Whilst there is empirical evidence that suggests that investors rarely benefit from timing the market, well-equipped active managers have also exhibited some degree of skill in bearish conditions. Despite such, the recent decade has proven to be difficult for active managers due to the rise of passive strategies. Passive mutual funds have garnered the ability to attract more than US$12 trillion in 2020, sapping out more than US$1.5 trillion from the active managers.

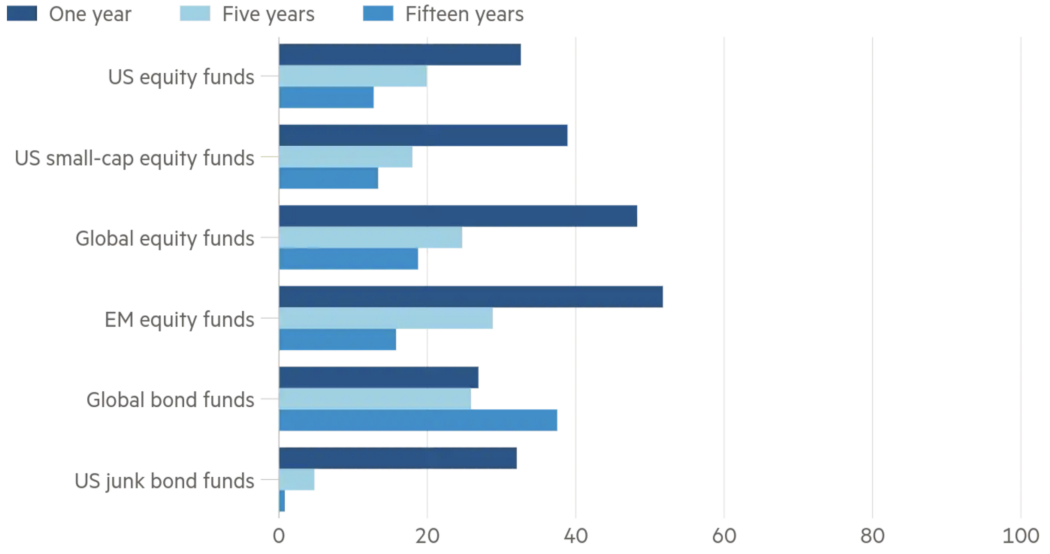

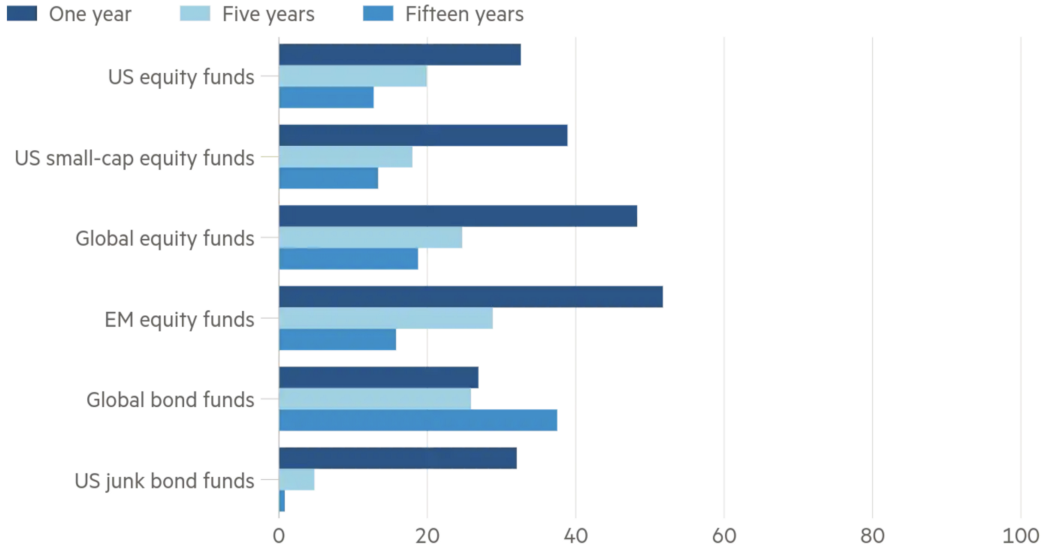

Figure 2: Percentage of funds which outperformed their benchmarks (Source: S&P Dow Jones Indices, 2020).

Figure 2: Percentage of funds which outperformed their benchmarks (Source: S&P Dow Jones Indices, 2020).

Active managers in the past decade have also struggled to beat their benchmarks. This waning confidence is reflected by the shift by institutional investors to swing towards passive strategies for a more cost-efficient means to generating consistent returns. Recent geopolitical upheavals together with the Global Pandemic, however, are expected to rejuvenate the active management globally to reinstate the value of generating returns via a manager. The resilience shown by active managers, considering the Pandemic, is a testament to actively managed funds to be able to survive industry tailspins. This has been true particularly for international equities and developing market funds.

Figure 3: Percentage of fees charged by asset managers by category from 1990–2020 (Source: Morningstar, 2020).

Figure 3: Percentage of fees charged by asset managers by category from 1990–2020 (Source: Morningstar, 2020).

Generating excess returns are not the only hurdle faced by active managers. Increasing fee pressures are plaguing managers globally, with active managers remaining the be the top pick to invite institutional investor scrutiny when it comes to fee-performance considerations. Large active managers have suffered consistent outflows in recent years (see Fidelity) despite managers beating the benchmark by an average of 3% a year for over three decades.

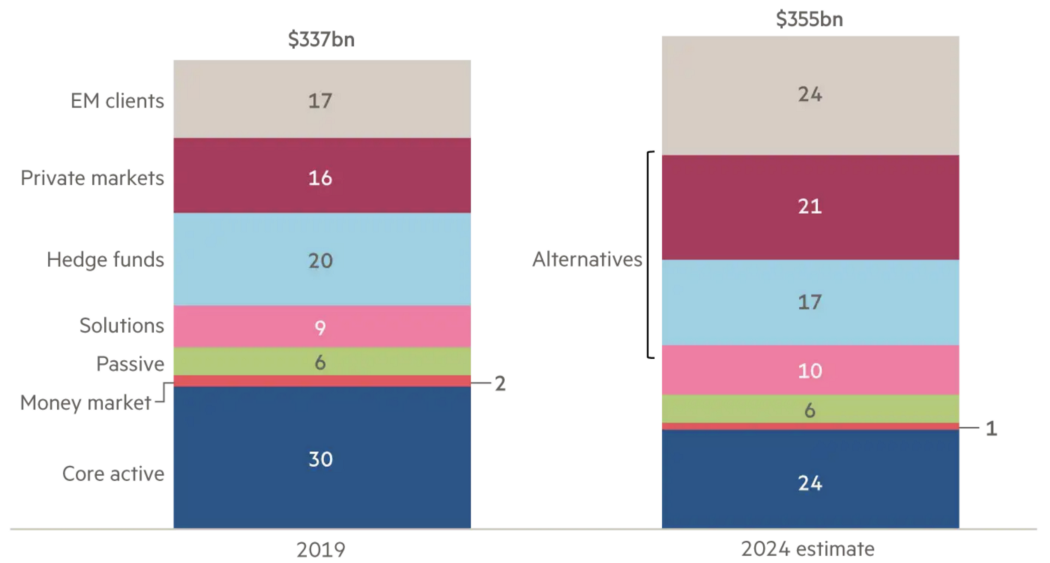

Figure 4: Market shares of investment categories (Source: Oliver Wyman, 2019).

Figure 4: Market shares of investment categories (Source: Oliver Wyman, 2019).

An industry-wide consolidation is inevitable for active management in the coming decades. Analysts opine that how active investors fare in the post-pandemic era would dictate the fate of the managers and advise cautious optimism moving forward for the industry. The discussion of scale and efficiency by active managers have been largely influenced by the shift in capital allocation to alternative strategies in active management, with an estimated 38% being allocated to hedge fund strategies and the private markets by 2024. This shift may also reflect the lofty expectations by investors unto managers in generating new, and perhaps, vastly superior performance via new techniques and methodologies.

The future of active management is uncertain based on how the cards are currently been dealt. One silver lining is the emergence of Smart Beta, which is an amalgamation of both active and passive management styles. Smart Beta strategies aim to deliver market-beating performance in a cost-efficient and transparent manner. The simplicity of Smart Beta portfolios is comparable to that employed by passive strategies but augmented to that of active management by selecting assets that exhibit return-generating drivers such as size, momentum, and value, all of which are proven to have performed well historically.

Whilst the prospect of Smart Beta seems promising, it might not be a panacea for all active managers. Tackling hurdles related to factor crashes from overcrowding (i.e., investors flocking to a concentrated group of assets) remain one of the large challenges for managers. To fully leverage the Smart Beta approach, managers will need to turn to quantitative methods and incorporate the use of cutting-edge technologies to identify pockets of Alpha and maintain optimal risks levels. Smart Beta remains a nascent approach for most asset managers, but its allure for managers to pivot towards remains appealing as it provides fertile grounds for active managers to reinvigorate its relevance in a post-Pandemic world.